Mean reversion.

Trees don’t grow to the sky.

Let your winners run.

Pigs get fat, but hogs get slaughtered.

There are all kinds of sayings about investing. Each may be grounded in some truth, but it’s fully possible to find sayings – and economists – who contradict in the moment.

Looking back, for example, 2023 was supposed to be a year of recession. A year in which the S&P 500 was predicted to drop per a Bloomberg survey of market strategists.

Source: CNBC.com

A recession didn’t happen, and the S&P has risen about 18% so far this year.

Why Small Cap Stocks Missed the Rally

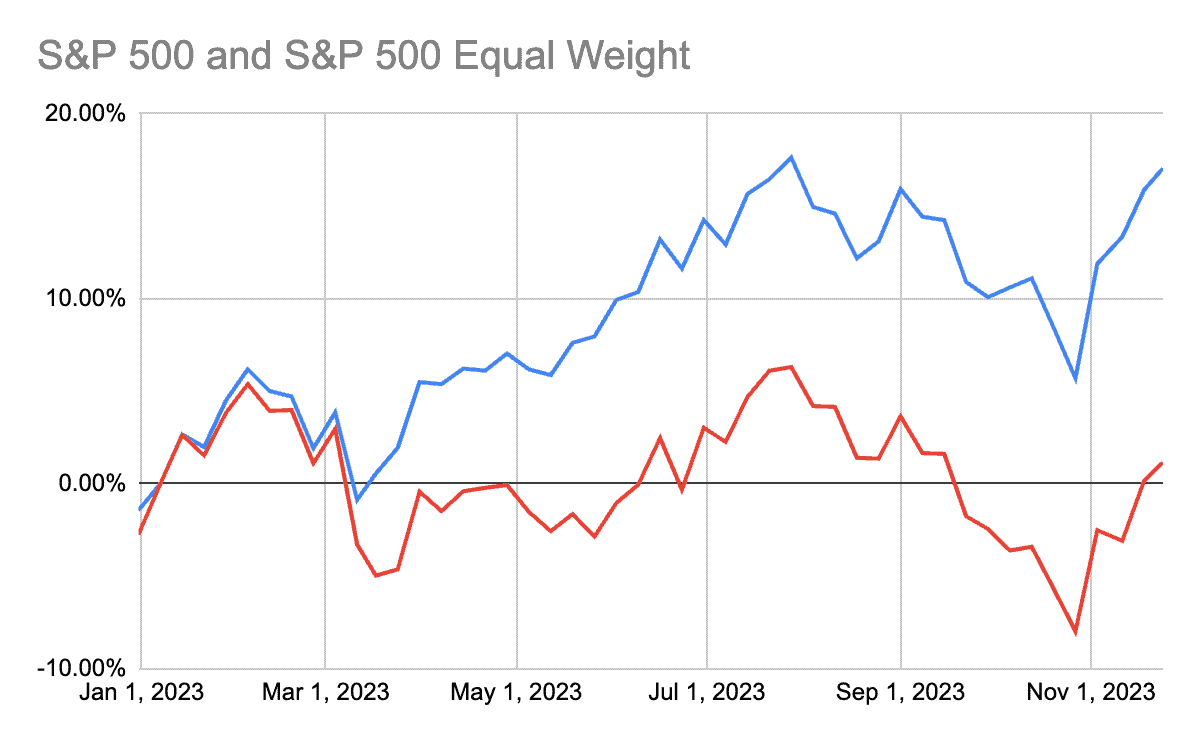

It’s always been a bit of an overgeneralization to talk about “the market” being up or “the market” being down. It’s not in the sense that plenty of investors own “the market” via an index fund, but it is in the sense that plenty don’t.

One anomaly stands out these days: the valuation gap between large and small firms. As you can see below, if we weight the S&P 500 stocks equally (instead of giving more weight to the biggest by market capitalization), the returns, in red below, are barely positive for the year:

Source: Yahoo! Finance

You may have heard the story: the stocks of seven big companies are heavily responsible for the S&P 500’s performance this year.

It’s true – and great for anyone who invested in those seven. (The S&P 600, for reference, is a small-cap index and has only gained about 0.5% for the year.)

Source: Google Finance

The most obvious, of course, is why.

The most obvious answer is that smaller firms, at least those based in the US, tend to have more debt than larger firms. (The Russell 2000 is also a small-cap index.)

Source: Bank of America/Merrill Lynch.

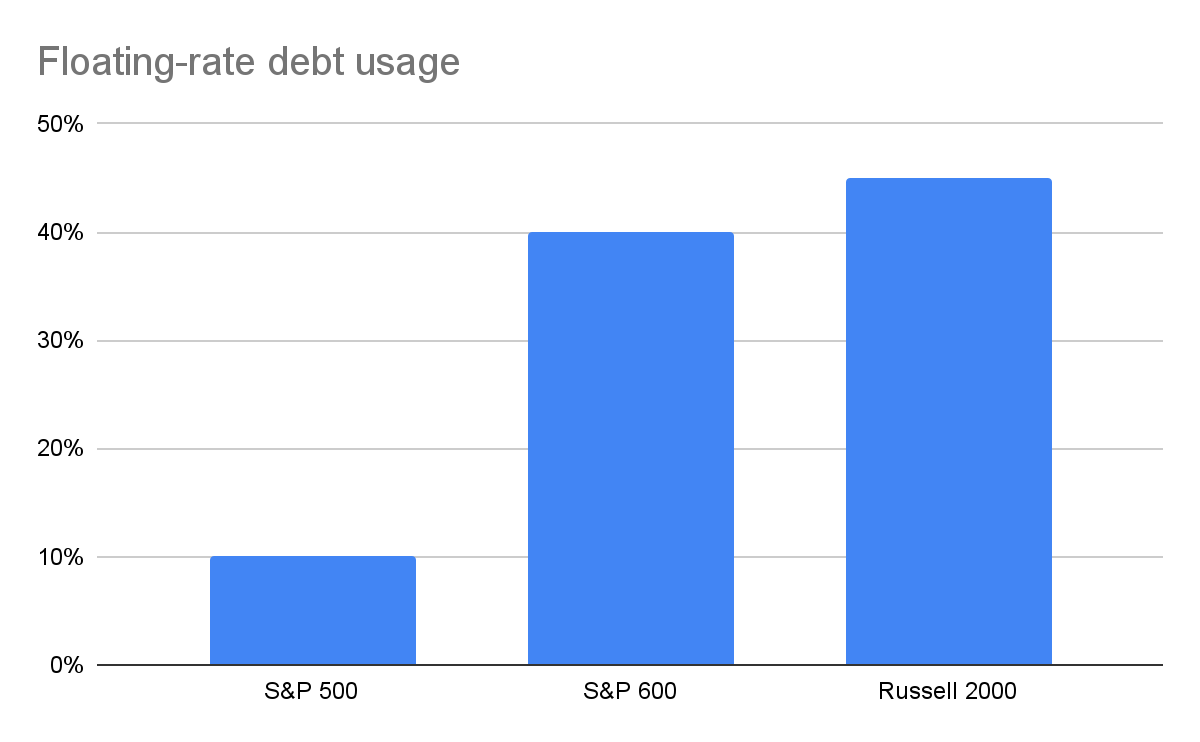

Moreover, for smaller firms, that debt tends to be at floating rates, versus at fixed rates, as the below chart shows.

Small firms, in other words, are affected more by rising interest rates than larger firms are. Larger firms, which tend to have stronger capital structures, wisely did a lot of borrowing a few years back when interest rates were low. In fact, in many cases, larger firms have been net beneficiaries of rising rates – because they’ve locked in fixed-rate debt at ultra-low rates, yet they’re earning more on their cash and short-term investments.

Data from FactSet, as cited on wsj.com and lazardassetmanagement.com

Even within small caps there’s a disparity: in this case, between value and growth. (Plenty of investors believe those distinctions create a false dichotomy – in a simple sense, investors are always seeking undervalued investments – “value” investing connotes finding slower-growing, often troubled, companies with low expectations that trade for even lower priced, whereas “growth” investing tends to mean paying higher prices for faster-growing, promising companies whose futures may be even brighter than the market expects.)

Data from Google Finance

Given that ultra-low rates were heavily responsible for a 13-year bull market in growth stocks in particular (in stock valuation models based on discounted future cash flows, low rates reduce the valuation difference – in today’s money – between cash flows expected to come soon and cash flows expected to come in the distant future; this effect offers a relative benefit to earlier-stage, less profitable firms whose hoped-for windfalls are far out), value was supposed to have its big comeback with the advent of higher interest rates.

Didn’t happen, thanks in part to excitement around AI.

Is it Time to Pile into Small-Cap Value?

That depends on your view on the US economy, and a few other things.

- Small caps do well with the US economy. Small caps have a reputation for doing well as the US exits a recession, and while a recession is still fully possible, a soft landing appears even more possible, at least according to surveys. Still, the logic is that small companies tend to sell more within the US, so a healthy or improving US economy benefits them relatively more than it does large companies, which tend to sell more abroad (about 43% of S&P 500 sales is overseas).

- Valuation gaps can close in two ways. The valuation gap between small and large caps is as big as it’s been in 25 years. Assuming we all believe mean reversion will close that gap at some point, we should commensurately keep in mind that it doesn’t have to be from small cap valuations rising (the optimistic way); it could be from large cap valuations falling, too (the pessimistic way). Or a mix.

- This time could be different. It almost never is, and these words are famously some of the most dangerous in all investing. New, value-adding things definitely emerge, but so many also-rans emerge, too, that the net effect to investors is often neutral or even negative. The US has seen more than 2,500 car companies come and go. Now we have three, arguably. But still, in the very long run, technology has turned human progress parabolic, and more people’s money is now parked in the stock market than ever before (and tax policies are more favorable for stock investors), so it’s possible that valuations could remain slightly higher than older averages, and that growth stocks could remain a bit more in favor than in historical times, when they were weird, fringe-y investments. Yet even if any of this is true, it would likely be closer to a gradual difference than a sea change.

It’s still heavily about interest rates

And remember: interest rates still have to come back down for a reversal of the aforementioned debt effect that’s likely the major ding on small caps these days.

I’m not giving advice – in this column, or in any – but while I’m always on the lookout for compellingly valued companies of any size, I tend to think that making any investments based on an anticipated capitalization-based mean reversion would be a premature move at a minimum.

Disclaimer: This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. Investing carries inherent risks. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.