2024: Double Average Returns? 24-Hour Trading, EV Stock Sink

Statistically, 2024 Should Be a Good Stock Market Year

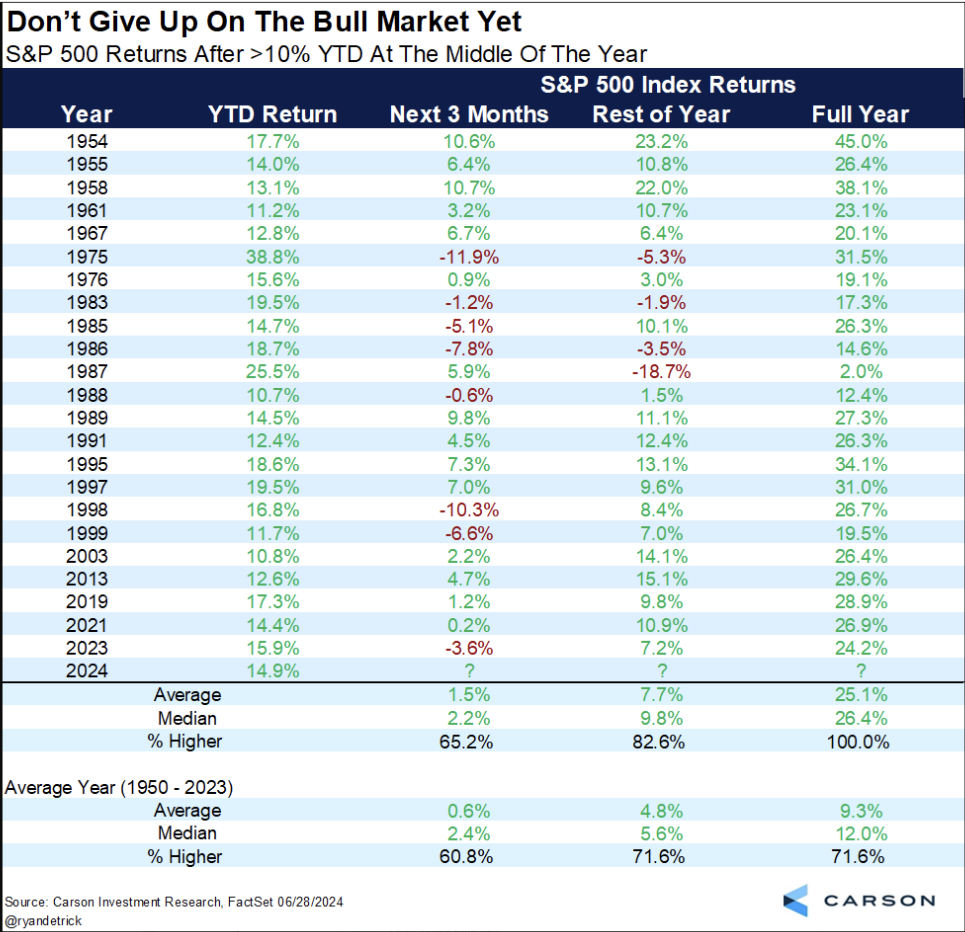

Our friend Enrique Abeya of HX Research shared a chart shared on X by Ryan Detrick of Carson Investment Research showing that when the S&P 500 has risen more than 10% in the first half of the year, the rest of the year has averaged 25.1%, versus a 9.3% average year.

In this case, there’s a lot of data, so I’d lean toward putting weight into this. It’s essentially a market momentum argument.

But this is a market.

And in markets, there are usually other opinions. JP Morgan, for instance, notes that big tech stocks have gotten overvalued, and accordingly, US markets could fall 23%.

Who’s going to be right?

This is a market. Nobody knows.

24-Hour Stock Trading

Bloomberg recently ran a piece on the increase in round-the-clock trading, mostly by retail investors (registration may or may not be required).

I can see a few ways of looking at this, each with its own legitimacy:

- It may be coming sooner or later. Younger retail investors are used to 24-hour trading from crypto markets, so equity markets that don’t have it might seem antiquated to them.

- It allows investors to react in real time to news.

- It’s good for international investors wanting to invest in the US. This is, to me, the strongest argument in favor of round-the-clock investing. That said, do domiciled exchanges have any implicit obligation to nationalism? If a US oil refinery has an accident in the middle of the night, investors in Asia, who are wide awake, will be able to trade on the news first. Does that disadvantage home-field investors? And if so, does it matter?

- It’s neutral for long-term investors. Back before we had zero-commission platforms like BBAE, I used a low-cost platform whose catch was that you could only trade on Tuesdays. Fine with me – I plan on holding for years, so waiting a few days is immaterial. Ditto for 24-hour trading. Not a needle mover for investors who care about future company economics.

- It’s bad for short-term traders and market professionals (as well as exchanges). Short-term-focused folks would say goodbye to the psychological release that came with the 4pm close. I’d argue that this is yet another reason to not invest for the very short term, but in fairness, many hedge and mutual funds (including long-term-focused funds) employ traders whose job is to get into and out of positions with minimal market impact. These folks may be small in number, but their lives aren’t made easier.

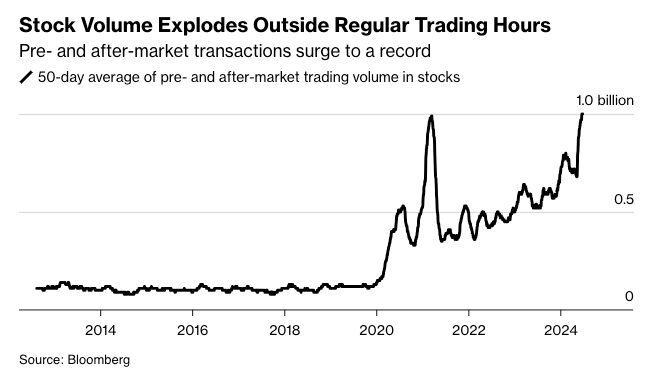

As the Bloomberg article notes, 12 billion US-market shares change hands daily (!), and the overnight trading volumes at Blue Ocean, the firm dominating overnight trading, is just 40 million. That 0.33% of daytime volume – rounding error.

But it may grow, and a chart for the same article notes that all-in pre- and post-market trading is considerably higher, at 1 billion shares per day:

As a long-term investor, I’m neutral on this, and probably see it as a net negative (for US-based investors) in that it tempts activity when none is probably needed.

Fun Fact: Essentially all the market’s returns happen after hours

I’d wonder about two things if overnight trading approaches meaningful volume. First is what might happen to the outsized returns that happen overnight. In 2019, Bespoke Investment Group showed that from 1993 to 2019, buying the SPDR S&P 500 ETF (NYSE: $SPY) at the market open and selling at the close produced returns of -13.9% per year.

That’s shockingly terrible. It’s even despite two big bull markets!

Meanwhile, buying at the close and selling at the open would have yielded 634.2%!

Not that I was following this strategy, but will it get traded away? In theory, more trading hours won’t change the amount of value in an economy or in a market – it just results in better or at least more frequent liquidity and price discovery.

Or does it?

The second thing I’d wonder about is to what extent overnight prices are “noise” prices (in academic parlance) or real reflections of real changes in company value. Does overnight trading just enable the wrong kind of investors using the wrong kind of investment thinking?

Again, I’m excepting non-US investors, and that’s a big and candidly unrealistic exception.

Forget about 24-hour trading – do we even need 9:30 to 4:00 trading?

Fun fact: Intraday trading isn’t very busy, even now.

As Matt Levine of Bloomberg mentions (again, registration may or may not be required, depending on how many Bloomberg articles you’ve read recently) most “real” trading – in the sense of price discovery and real auctioning – happens in the first minute or so of the trading day. That’s when the actual investors are trading with each other. Market makers (who are more focused on providing liquidity than price discovery) facilitate much of the volume outside the busy open and close moments. (NB: An exception would be if a truly market-moving event happened during a trading session.)

More simply, even now, despite a 6.5-hour trading day, the “real” trading is confined to a few moments each day. Even on the biggest and busiest stock exchanges in the world – when the major trading participants are awake and on the job – most of the trading time is borderline useless. There’s an argument that we don’t even need trading from 9:30 to 4:00.

Do we really need to extend trading hours? In fact, what if we went the other way?

What if stocks just had one brief auction period every day in which a daily clearing price was established? Mutual funds roughly do this, and everybody lives. (They could still set their NAVs after the equity prices get established, as they currently do.)

We’d save a lot of time and energy that could probably be put to better societal use. Investors outside the US wouldn’t have to stay awake to monitor ongoing trading sessions. And we’d focus everyone on longer-term company economics, instead of day-to-day trading minutiae, which is what really matters anyway.

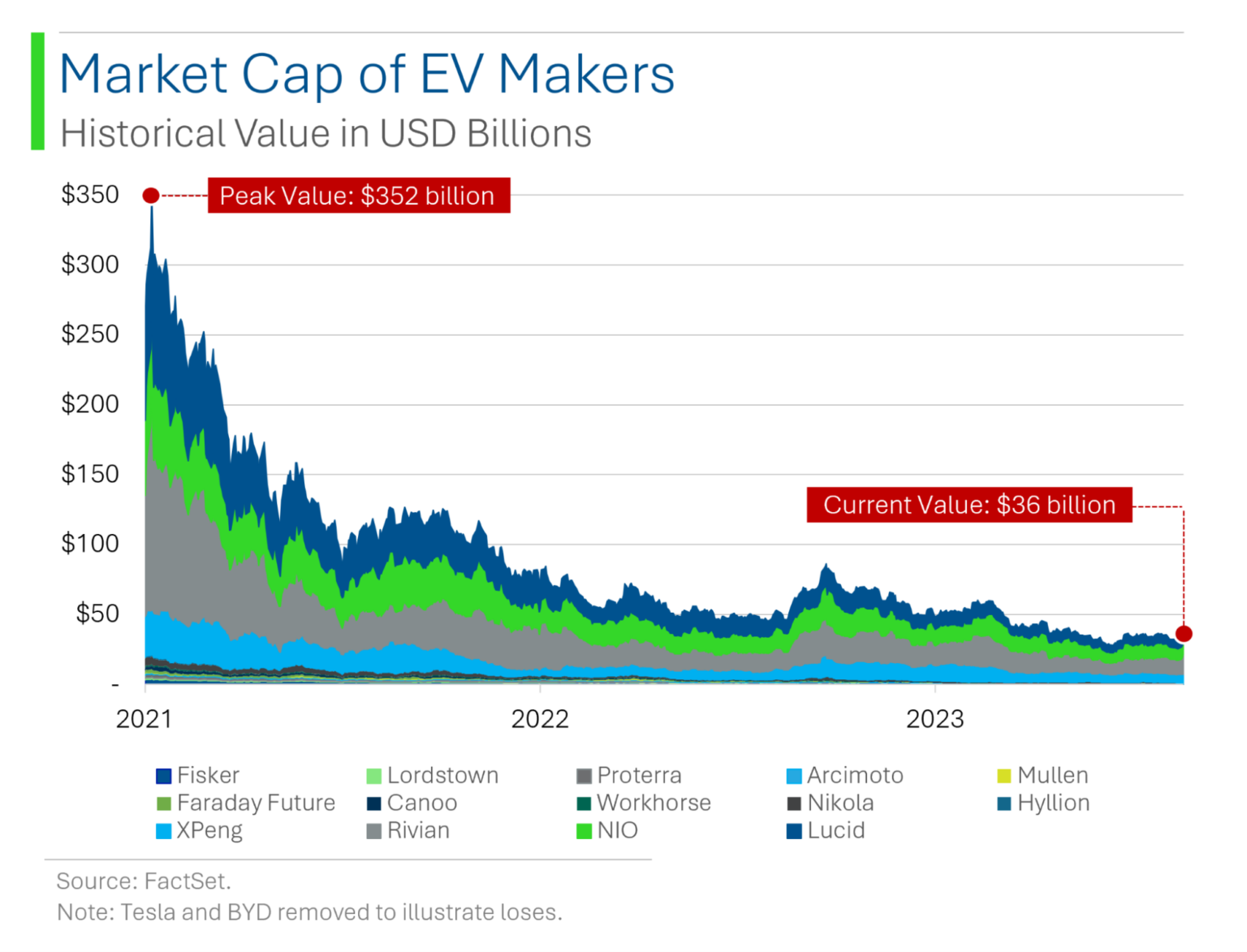

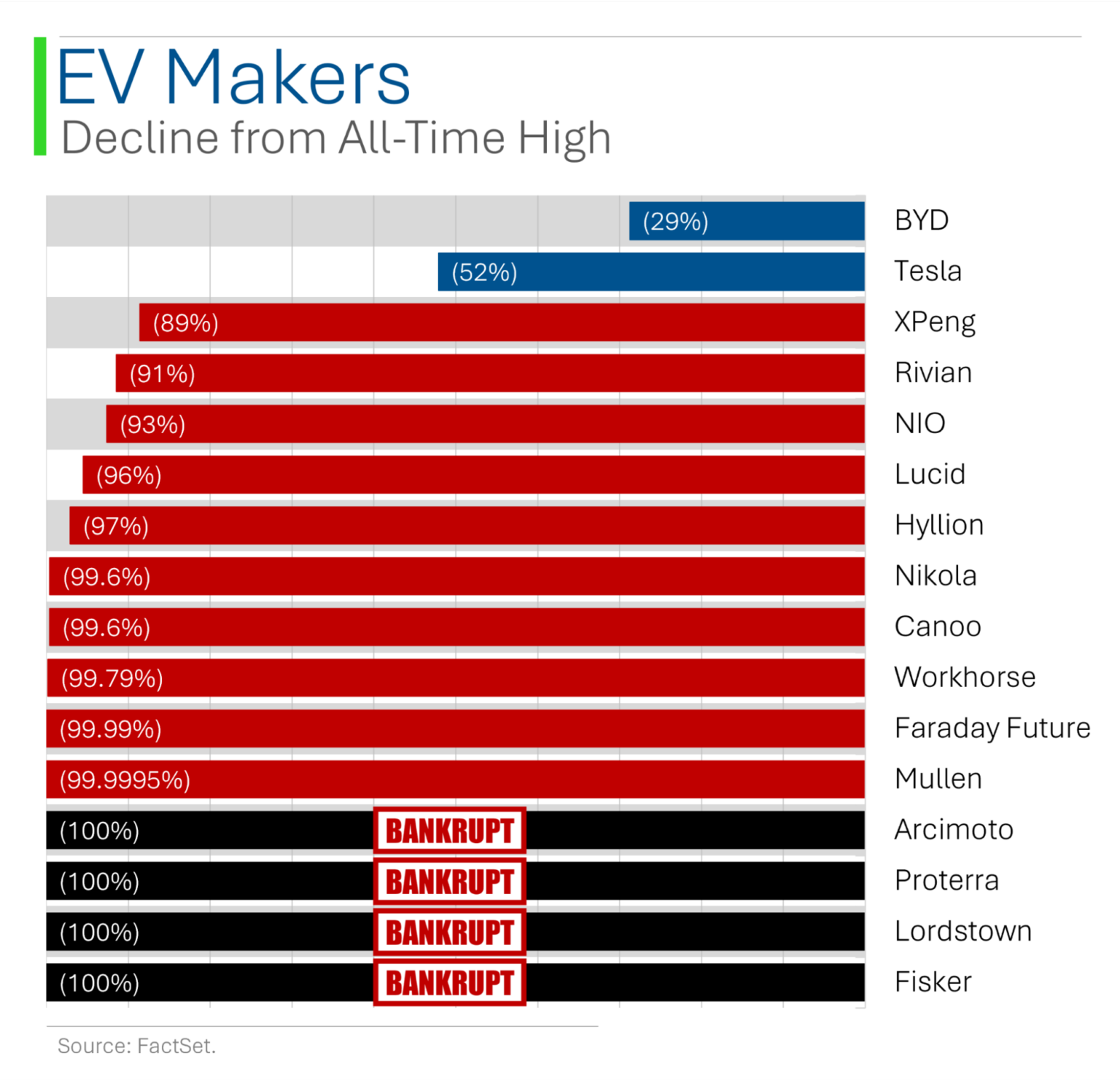

EVs Stocks Have Plunged

Another shout-out to Ryan, writer of StreetSmarts by MarketLab, who has a way with visuals. In this case, the visuals basically tell the story: EV stocks have gotten killed since their 2021 peaks.

Note two exceptions, which Ryan notes he’s left off the first chart: Tesla and BYD.

Of course, Tesla, even after a halving, has been a fantastic investment over the long haul, which is one truth. The other is that just about every other EV maker hasn’t.

This doesn’t surprise me. I predict that something similar will happen with AI: A few big winners surrounded by plenty of losers. This is how industries evolve. It’s also why academic studies show that growth investing is so hard. We tend to see the survivors, and tend to read stories about people who made fortunes investing in the survivors, but for every Tesla and BYD (which isn’t fully an EV company, incidentally), there are plenty of also-rans.

These charts may beg the question: Are there bottom-fishing opportunities? There may well be, but judging by the tendency of these companies to run out of cash, I’m not rushing to buy myself.

Poster available at Despair.com

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. James owns shares of SPY. BBAE has no position in any investment mentioned.