This Stock Market Has More Momentum than Ever (Literally)

Much has been made about the fact that stocks have been going up. As investors, we welcome that.

Well, mostly. To be precise, we welcome it if we already bought stocks; if we have not yet bought, we should celebrate when they go down, to paraphrase Warren Buffett, because they become cheaper for us to buy.

Most investors have both motivations: an existing portfolio, best served by price rises, as well as an intention to buy more stocks as time goes on, which is best served by price declines. The relative weight of those motivations changes with age (or maturity of one’s nest egg): younger investors whose main stock buying are ahead of them should get more excited about price declines, whereas retired investors who aren’t adding new money should cheer price rises.

Of course, it doesn’t work like this in real life. Everyone cheers price rises. But this is the theory.

The current US market is the most “momentum” market ever

Stock market momentum is defined as the upward trajectory of prices – over hours, days, weeks, months, or even a year or more. There’s a whole science to it that I’ve only obliquely encountered, and probably some pseudo-science, too, but 10-day, 50-day, 100-day, and sometimes 200-day momentum-related measures are probably most common, with 6- and 12-month momentum appearing more in academic literature than practice.

(Speaking of science, stock “momentum” is, in some respects, closer to inertia in physics; physical momentum is mass times velocity, which might map closer to something called volume weighted average price, or VWAP, in stock investing.)

Momentum is a factor, and if you’ve been reading the BBAE Blog for a bit, you know I like to talk about factors: the academic term for reasons stocks go up and down.

Factor performance is imputed. If you only had one stock in the world, it would be hard to know which factors were responsible for performance, except in obvious circumstances. But since we have many stocks, we can look at patterns – which types of stocks are going up and which are going down – and impute the factors the market loves more and less at any given time.

And right now we are in a momentum-driven market – as “momentum” as it’s ever been, in fact. See this graph shared by John Authers of Bloomberg:

One interpretation is that a momentum market is a bit of a “Greater Fool” market – investors are buying because other investors are buying, and placing less relative importance on company fundamentals.

(Side note: look closely at the left graph above – it starts in 1972, and since then, the S&P 500 Momentum Index (which basically finds the top 20% of S&P 500 stocks by LTM, and then cap-weights them) has become a bigger and bigger outperformer of the regular market cap weighted S&P 500. Note also that its relative performance – the “vol of the vol” as we used to say in the hedge fund world to describe the derivative of volatility – broadly appears to be increasing as time goes on.)

With all the focus on momentum, who’s been losing?

John’s second graph shows that it’s value:

Ok. But how much is temporary and how much is permanent?

One one hand, we had a global financial crisis, and we had 13 years of freakishly low interest rates. It’s fair to say that the past 16 years have been atypical for stocks.

On the other hand, if you were to take a snapshot of human progress, showing civilization now, 5 years ago, 50 years ago, 500 years ago, and 50,000 years ago, you’d see that not only have humans progressed, but, generally, the rate at which we’ve been progressing has been increasing (another second derivative concept, for the math nerds). As I mentioned in a prior post, this time is different in stocks to some degree.

I don’t have the answer. I only have the question, which is: What’s the new baseline going to be whenever things finally “settle down?”

Momentum investing seems to actually work

I’m not a momentum investor. The idea of just buying something because everyone else is buying it has always felt a bit too mindlessly herd-following-ish to me. But academic studies look kindly on momentum (and on value investing, which seems almost like momentum’s opposite, but less so on growth investing and technical analysis).

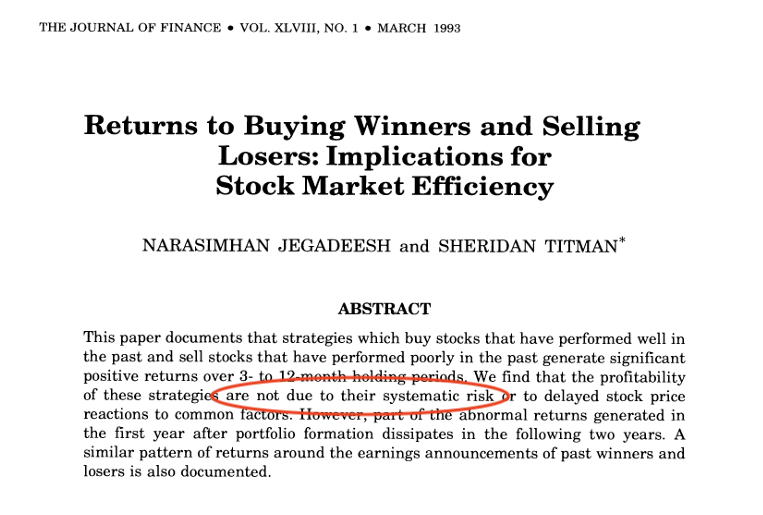

A 1993 paper by Narasimhan Jegadeesh and Sheridan Titman called “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency” is a seminal work in momentum investing. It showed a strategy that could have earned 12% of compounded excess returns per year. (In excess of what the returns should have been for the risk taken, according to then-prevalent financial theory.)

This was the heyday of the Efficient Market Hypothesis (EMH), and the idea of some profitable anomaly existing without being traded away deeply perturbed financial academics, so the paper partly battles the prevailing EMH wisdom while simultaneously promulgating momentum. A key point of the Jegadeesh paper was explaining that momentum’s results were not due to an inherent additional riskiness of the momentum strategy:

That paper has been cited more than 16,000 times – Hall of Fame-level for financial academic literature – and its results replicated, dissected, and critiqued.

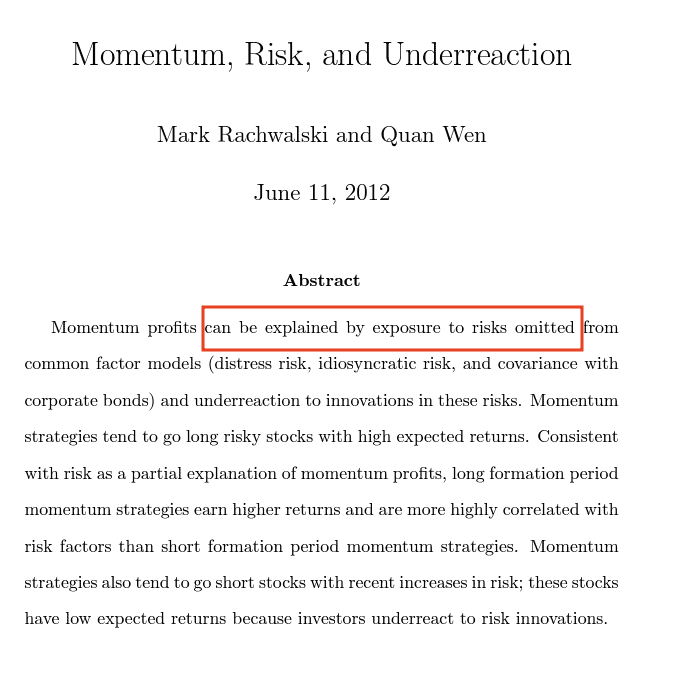

The main critique – summarized in the below paper (which seems to have gotten just one citation, per SSRN.com) – is that momentum does well because it embeds additional risk, and that risk is just harder and weirder to measure.

Should you follow momentum investing strategies or not?

I am not here to tell you what to do. I don’t debate the positive tilt of the research; if you can make money with momentum investing, do it.

But – and this is conjecture – because other research finds a tendency for people to buy at the top, I’d guess there’s a decent Average Joe-risk of buying late into a trend, after a really long period of demonstrably positive momentum, In 2021, for instance, more money went into US equity markets than in the prior 19 years combined. Momentum latecomers risk buying at the top but, of course, whether a trend will last for 6 months or 6 years can only be known in hindsight.

Separately, if you’re a civic-minded, consider this thought experiment:

If every investor invested based on fundamental analysis, we’d have far less volatility (which would increase equity values), and equity markets would do a better job of improving economies by allocating capital to deserving companies while keeping it away from less deserving ones. A market full of Warren Buffetts makes the world better.

Conversely, if every investor invested based on momentum, we have extreme boom and bust cycles, and valuations would swing far from economic reality. The equity market becomes a casino. Investors only put “gambling” money in, keeping their retirement money somewhere else. Companies no longer feel fairly rewarded by markets and seek to list somewhere more rational, or just not list at all.

Which future do you want to contribute to?

Momentum investing is a bit like freeloading: A few people can do it, but if everyone does it, things deteriorate – for everyone.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.