Weekly Roundup: Rate Drop Delay, Corporate Profits, Real Estate

Welcome to your weekly BBAE Roundup! Over the next several weeks I’ll be exploring ways to make this roundup as ideal as possible for our readers, so expect a few tweaks here and there. I’ll start by connecting this week’s news more closely to the foundational principles underlying the headlines.

James

Stories this week:

- Stocks Drop on Slow Interest Rate Cuts

- Small Caps Coming Back in Style

- Real Estate Woes

- Online Economic Survey Results Are More Extreme

Stocks Drop on Slowish Interest Rate Cut Forecast

I actually had some different topics for this week, but Thursday’s market movement – the S&P 500 dropped 1.4%, with the follow-along SPDR S&P 500 ETF (NYSE: $SPY) dropping another 0.35% after hours – took center stage.

Interest Rates

Central banks raise interest rates to slow overheating, high-inflation economies – high interest rates increase borrowing costs (making borrowing money less attractive) and, a more wonky effect, they also reduce the value of companies by raising discount rates in equity valuation models (the present value of $1 expected a year from now gets lower as the discount rate gets higher).

Following 9% inflation (a delayed reaction to ultra-low interest rates prior), the US Federal Reserve hiked interest rates by roughly five percentage points in what I believe is the steepest rate hike period, ever.

The Fed had plenty of doubters, who felt inflation was untameable, but the consensus now is that hiking was the right move – it brought inflation down (to around 3% now, which is still above the Fed’s 2% target but getting close), but stocks didn’t suffer.

With the mission largely accomplished, the debate has turned to when and how fast the Fed should start lowering rates.

Why? Good question. The US economy is still in excellent shape, with strong employment, strong household finances, and a record-setting stock market. But it’s starting to slow – a desired consequence of the high rates – and because there’s a time lag with these things, the Fed worries that if it doesn’t start bringing rates down soon, the economy will start slowing too much.

It’s kind of like correcting a boat, or at least a car driving on ice, versus a car on pavement: Gentle and gradual is the name of the game.

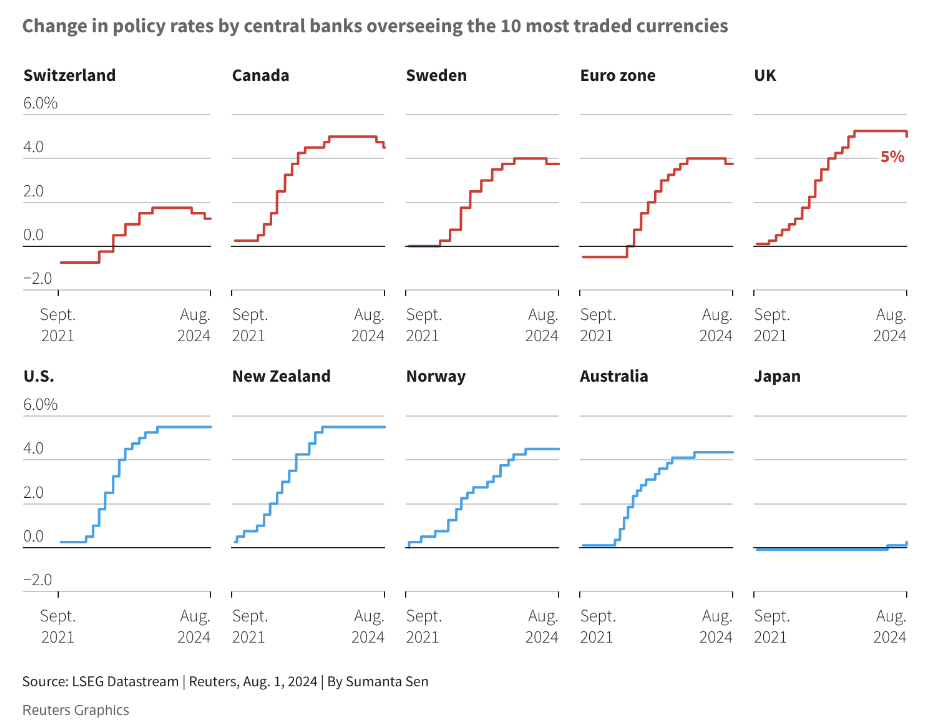

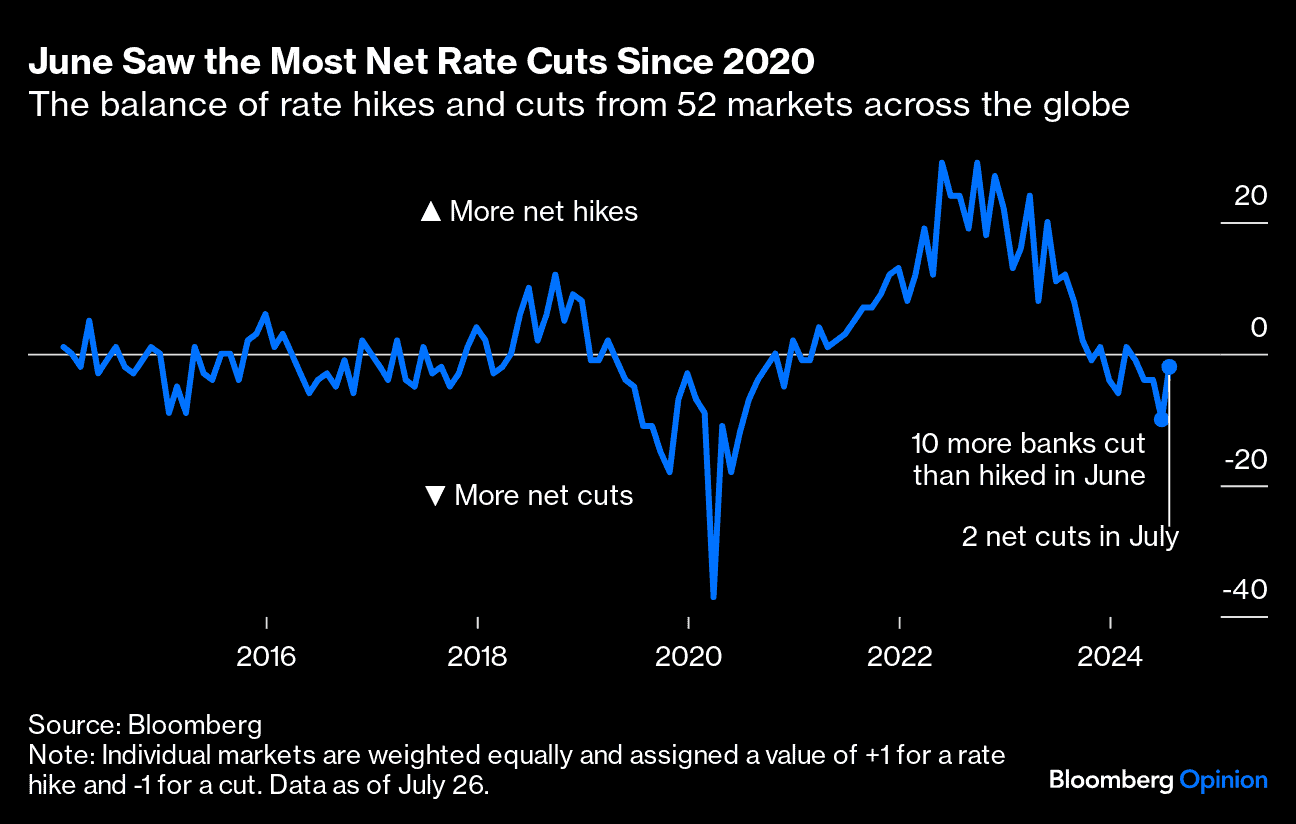

And both the UK and Eurozone central banks recently cut rates, as did a few smaller banks, so eyes have been on the Fed (in fact, as of last December, investors were expecting the Fed to cut rates at least seven times in 2024; so far, we’ve had no cuts).

Bloomberg put out a similar graphic, even before the Bank of England joined the cutting party.

So basically, the Fed has been keeping rates higher for longer than expected – not good for stocks – and on Wednesday, Jerome Powell sounded wishy-washy about further cuts, only saying that a September rate cut “could be on the table.”

This sounded too close to “higher for longer” to the market, which punished stocks.

But not all stocks.

In some ways, we saw a more extreme version of the “out with the sexy, in with the boring” trend we’ve been seeing.

Dividends in particular seem back in style.

The Dow Jones Utility Index, for instance, actually rose 2.31% on Thursday, and the Dow Jones All REIT Index rose 1.33%. (Utilities and REITs tend to be safer, steadier companies that pay big dividends.)

The hot-until-recently NYSE Semiconductor Index plunged 7.26%. Ouch.

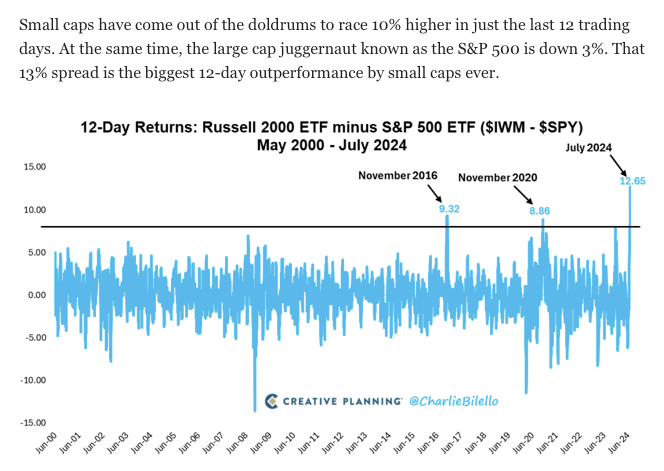

Small caps also got hammered, with the small-cap Russell 2000 Index down 3.03%. This was actually a reversal of the mini-revival that began a few weeks before the Fed meeting. The graph and text from Charlie Bilello – which Charlie put out before Wednesday’s Fed meeting – explain it:

Not anymore. Small companies tend to have a lot more debt, and a lot more variable rate debt than large caps, so “higher for longer” means more pain for them.

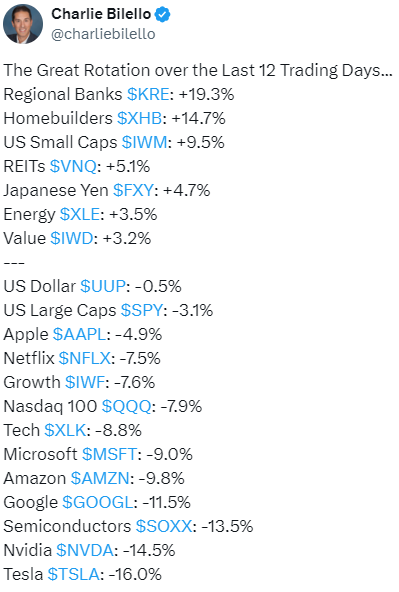

Another made-before-Wednesday Charlie post shows how quickly high-flying tech stocks have come down:

Granted, they still have plenty of gains to give up. But with the momentum against tech (which was arguably in a bubble) and interest rates against small caps, steady dividend payers may indeed remain a refuge.

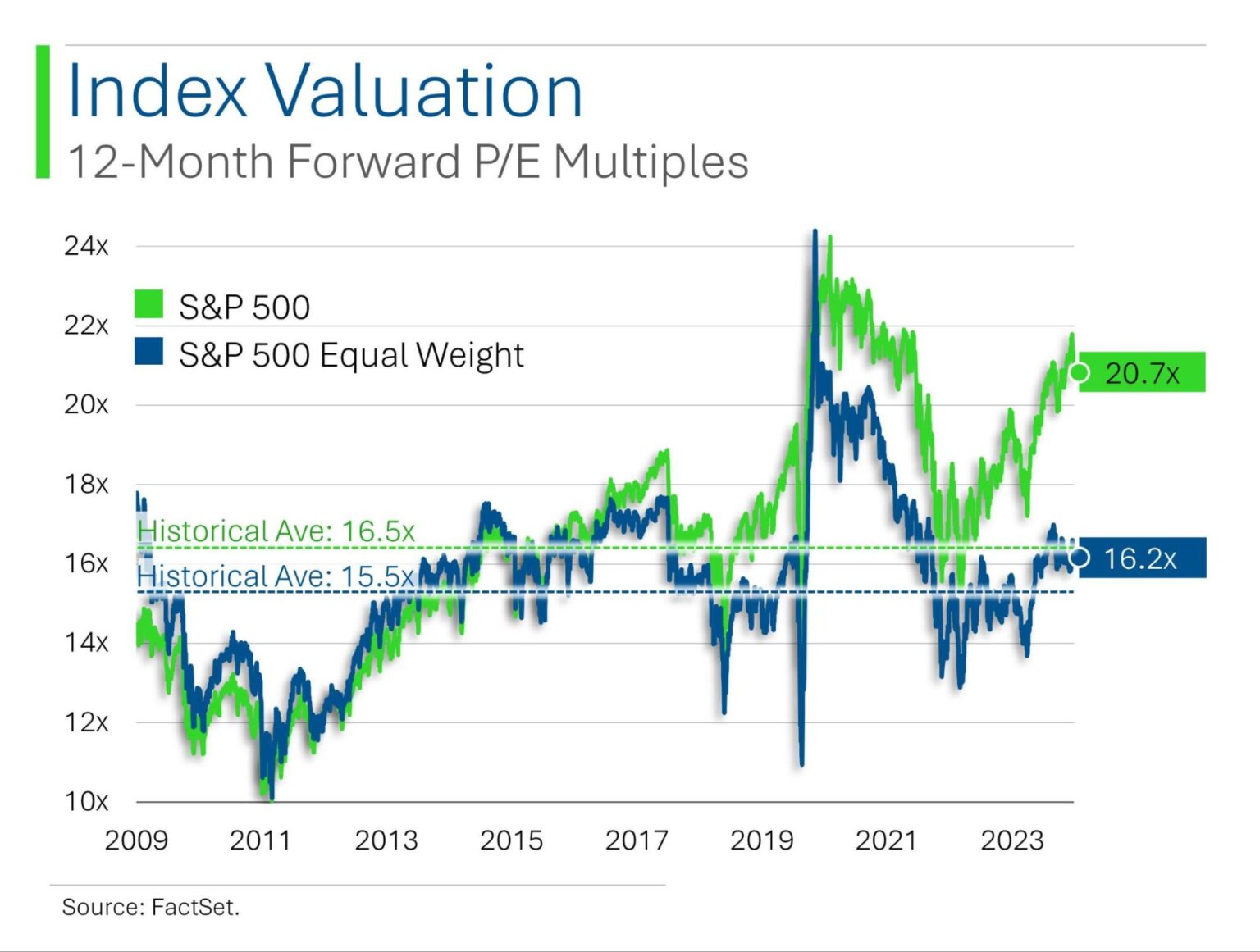

A pity, because the “buy small caps” theme was gaining serious momentum up until Thursday. While the equal-weight version of the S&P 500 isn’t terribly small-cap-ish, it does massively lower the “voting” power of the top-heavy tech stocks (Magnificent 7, plus some semiconductors and other tech). While this StreetSmarts graphic was produced just before Thursday’s rout, it shows how much cheaper the equal-weight market is.

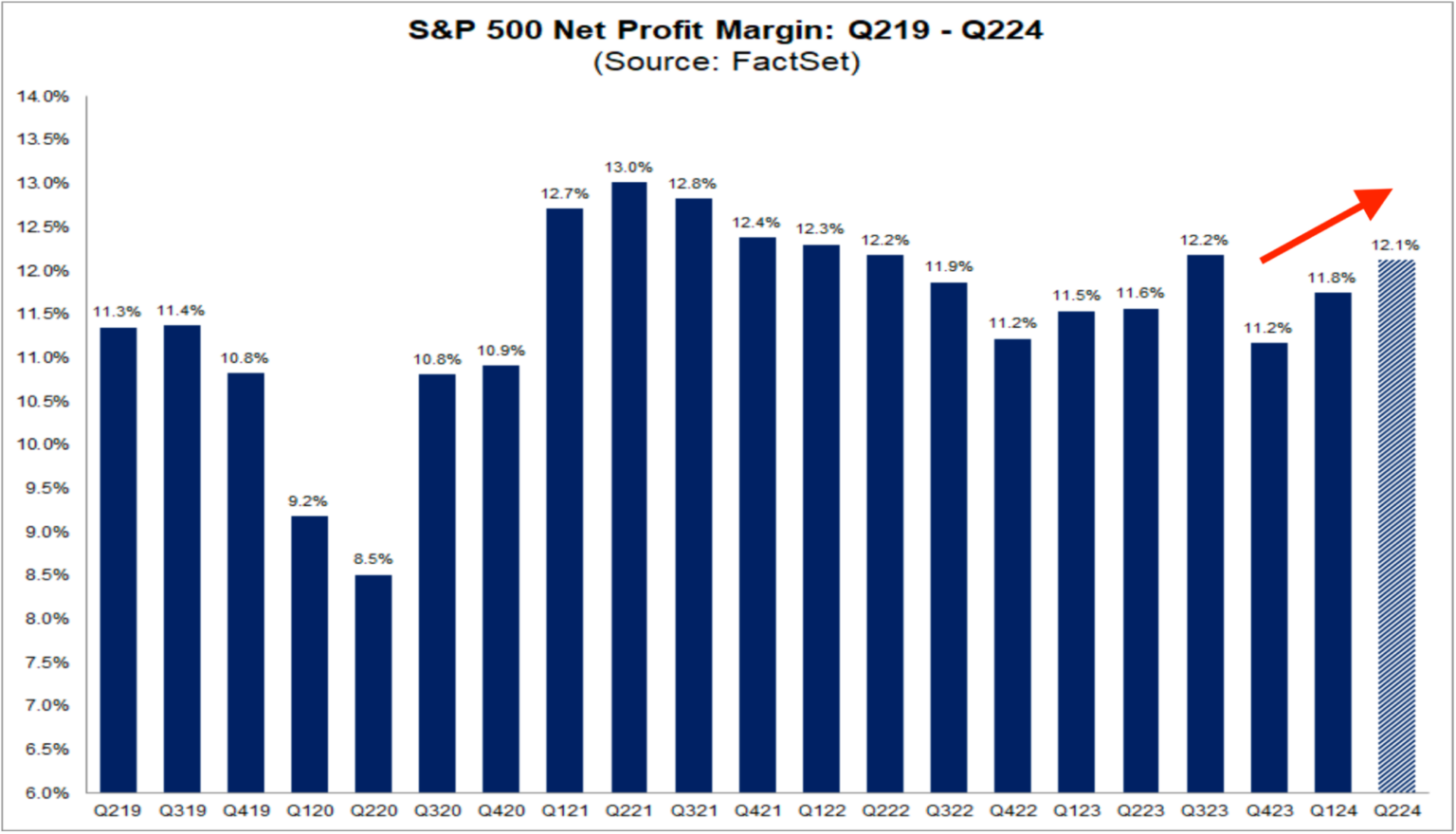

Corporate Profit Margins are Rising

This would normally not be a story if inflation weren’t falling, if the unemployment rate wasn’t rising, if home sales weren’t slowing – if the US economy weren’t softening, in other words.

Sam Ro of Tker.co has a good piece about this (sharing a graph from it below).

It’s just odd. If you’re new to profit watching, it’s good to see companies make more money – profit is the financial raison d’etre of a business, and stock prices tend to map to profits.

The question is: Why, if the economy has been softening, are profits rising?

Sam leans toward the hypothesis that corporate operational efficiencies long in the making are finally taking effect, continuing to improve results despite softening elsewhere.

To channel Matt Levine: I guess?

There is some reason this is happening. And the economy has been a show of conflicting data points for the past few years (conflicting, though mostly good). So this is one more.

The positive for investors: It’s hard to picture stocks falling too far when profit margins are rising.

Commercial Real Estate Keeps Tanking

We mentioned this before, but it keeps on playing out exactly as expected. In this case, a New York City office building that sold for $332 million in 2006 just sold for… drumroll… $8.5 million. Here’s The New York Times article on it (I’m trying the “gift this article” feature, but registration may still be required, and if you can’t see it, don’t worry – the idea is simple).

This makes me scared of commercial real estate firms, as well as banks.

Now, arguably, with interest rates falling, banks may not do as well. Warren Buffett has been selling off his Bank of America (NYSE: $BAC) holdings. But real estate tends to be more local, and officially recorded transactions like the above set comparable valuations that negatively affect bank loan collateral.

In other words, if Local Bank lends to Local Commercial Building Developer so he can build his fifth building, the loan covenants will stipulate the developer (or ultimate building owner) maintain a certain baseline of collateral, likely in the value of the project (especially for big projects) or potentially across projects if it’s a smaller developer in smaller region. The bank just wants to know it can lay claim on some valuable assets if the owner can’t repay the loan. With fewer people using offices, owners have lower cash flows, and with these fire-sale valuations, their buildings – even if they do generate robust rental income, which they probably don’t – aren’t worth as much. This stresses the local banks – and local bank investors.

The reflexive counterargument is that this story is known and presumably baked into bank stock prices by now, and that if things end up less bad than expected, smaller bank stocks could soar. Maybe. But with a New York City office building selling for $8.5 million, I’d be afraid to take that bet.

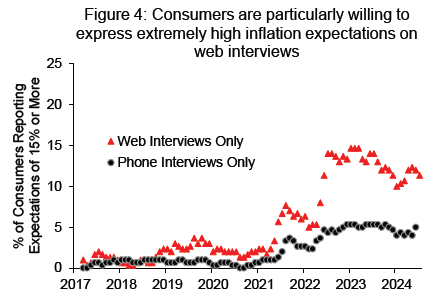

People Are More Extreme Online

A University of Michigan comparison found that when asked on the phone about how much inflation they expect, people answer more moderately than they do when given a web survey.

It makes sense, I suppose. People tend to be herd-seeking, herd-forming, and mean reverting, as any parent of a teenager knows. It’s a species survival mechanism. There are positives and negatives about this for society. More time spent digesting algorithmically served social media content instead of watching the same mainstream media channels Gen Xers like me all watched growing up likely means more extremism. But I’m not sure that stifling one’s true economic views – presumably out of self-consciousness around having “way out there” expectations – is a positive. Getting true answers has long been a challenge in sex surveys – and, apparently, in economic surveys, too. We just didn’t know it.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. James owns shares of SPY, BBAE has no position in any investment mentioned.